Note: This article can be found on my substack https://cammmwatson.substack.com/p/japan-biosolutions-the-growth-stage

Japan is an unusual biosolutions story: mature, applied, industrially embedded, and largely overlooked in the conversations dominated by the US and China.

The patents are there. The corporates are engaged. The downstream demand is real. Japan also has something less obvious: deep manufacturing reach across Asia Pacific, built over decades of industrial embeddedness in chemicals, materials, food, and manufacturing. These are precisely the sectors where biosolutions are heading.

What’s missing is the connective tissue between validated ideas and industrial scale. Not one thing, but three: growth-stage capital and risk ownership, industrialisation infrastructure (GMO-ready facilities, downstream processing capacity) and the distributed operator capability that only comes from actually running these processes at scale.

This is the “missing middle,” and it’s the defining structural feature of Japan’s biosolutions ecosystem right now.

The pattern that results is predictable: early liquidity events, firms drifting toward deeper capital markets, corporates cycling through pilots and minority investments that never quite tip into commitment. The corporate appetite is genuinely there but appetite without a shared playbook for coordination doesn’t move the needle.

From the outside, the transition gap looks like the interesting space. Not more early-stage funding. Not more pilots. Coordinated, patient, growth-stage mechanisms that align capital, corporate adoption, and industrialisation infrastructure. That’s where the value creation appears to be. And it’s largely unclaimed.

For startups, that reframes what Japan is. Less a formation ecosystem, more an adoption gateway worth engaging early. For corporates, the unlock seems to lie in coordinated structures that share first-mover risk rather than isolated pilots. For investors, the growth-stage coordination gap looks like the investable space; underwriting transition to scale rather than company formation alone.

I’ve spent most of my career working with US and UK-based biotech startups, which shapes how I see ecosystem structure, what enables companies to scale and what gets in the way. I’m currently based in China, another ecosystem with its own distinct logic, which makes Japan’s structural choices all the more visible by contrast. This report draws on patent data, deal analysis, interviews, and ecosystem mapping carried out in collaboration with OneNucleus, Potter Clarkson Law Firm and the UK and Japan BioIndustry Associations.

1. What the company landscape looks like

The summary above sets out the headline argument. What follows is the full picture; the data, the deal patterns, the corporate behaviour, and the structural logic underneath.

Japan has a mature life-science services base, including CROs, CDMOs, CMOs, and analytical providers, reflecting decades of pharmaceutical-driven capability. Its biosolutions company base remains modest but emerging, concentrated in agricultural, food, and industrial domains.

Biotech and biosolutions service capacity:

Against this backdrop, Japan’s biosolutions company base remains modest but emerging, with activity concentrated in select application areas.

Biosolutions company landscape:

2. Where the innovation is and who owns it

At the level of upstream innovation, Japan shows high and sustained activity across biosolutions-relevant synthetic and engineering biology. This strength is visible not only in aggregate patent volumes, but in the range of application domains and the types of organisations generating that IP.

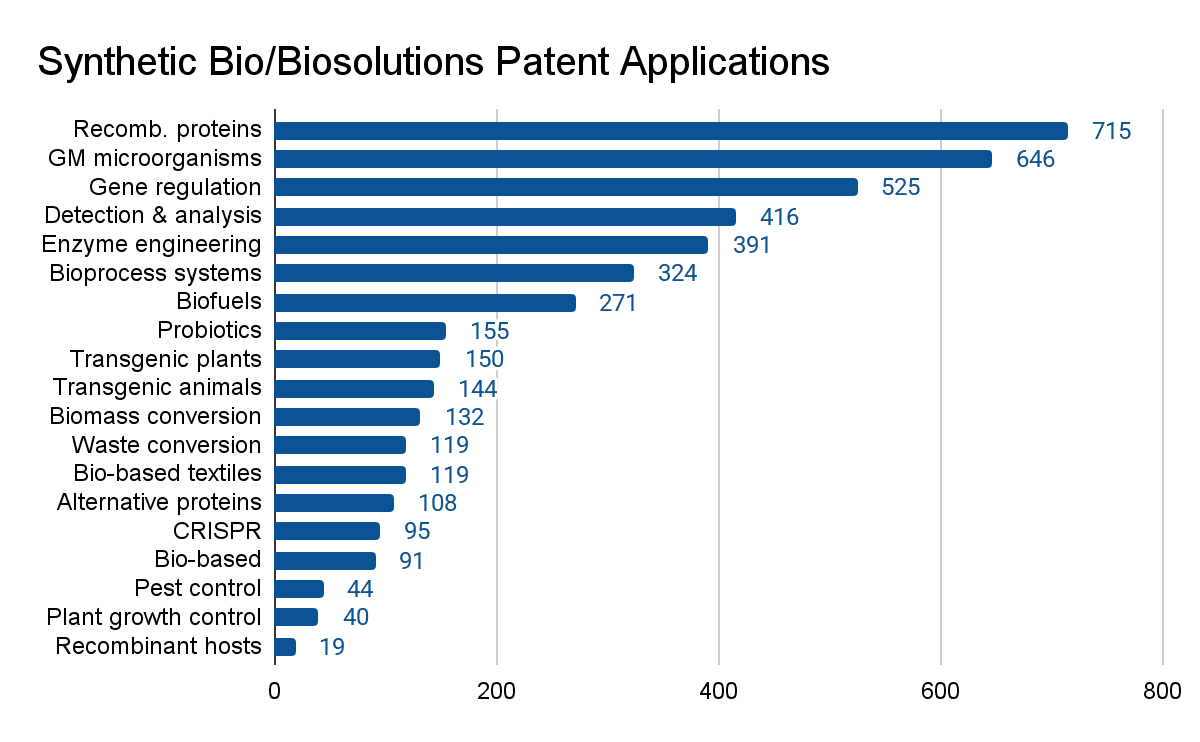

2.1 What is being patented: applied biosolutions domains

Patent topic analysis indicates broad activity across non-therapeutic biosolutions areas (2004 to 2023). In these domains, early intellectual property may have limited standalone value; commercial impact is realised only when biological performance, process engineering, and manufacturing are integrated at scale.

Looking at assignees, biosolutions IP in Japan is concentrated among large corporates and public research institutes, rather than early-stage startups.

Biosolutions IP accumulates primarily within organisations that already operate at industrial or quasi-industrial scale. This structure favours applied problem-solving and incremental capability building, but does not naturally produce independent, fast-scaling companies. The issue seems not to be an absence of innovation or corporate engagement, but the absence of a clear institutional owner for scale risk, coordination, and long-horizon capital commitment.

Representative top biosolutions patent assignees from 2004 to 2023:

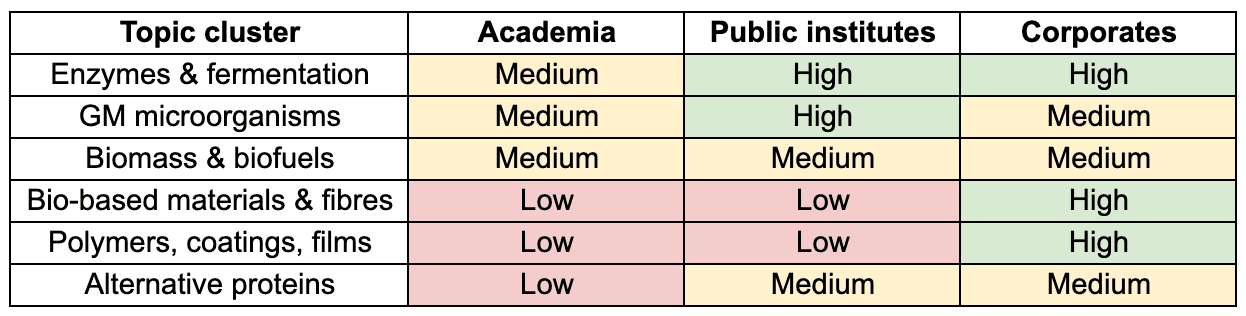

Breaking patent activity down by type of patenter reveals a consistent division of labour:

Corporates dominate downstream, application-heavy domains (materials, polymers, coatings, films).

Public institutes play a strong role in enabling layers (microbial platforms, enzymes, processes).

Universities are present across domains but are less dominant in application-intensive areas.

2.2 Early translation: what NEDO-supported projects show

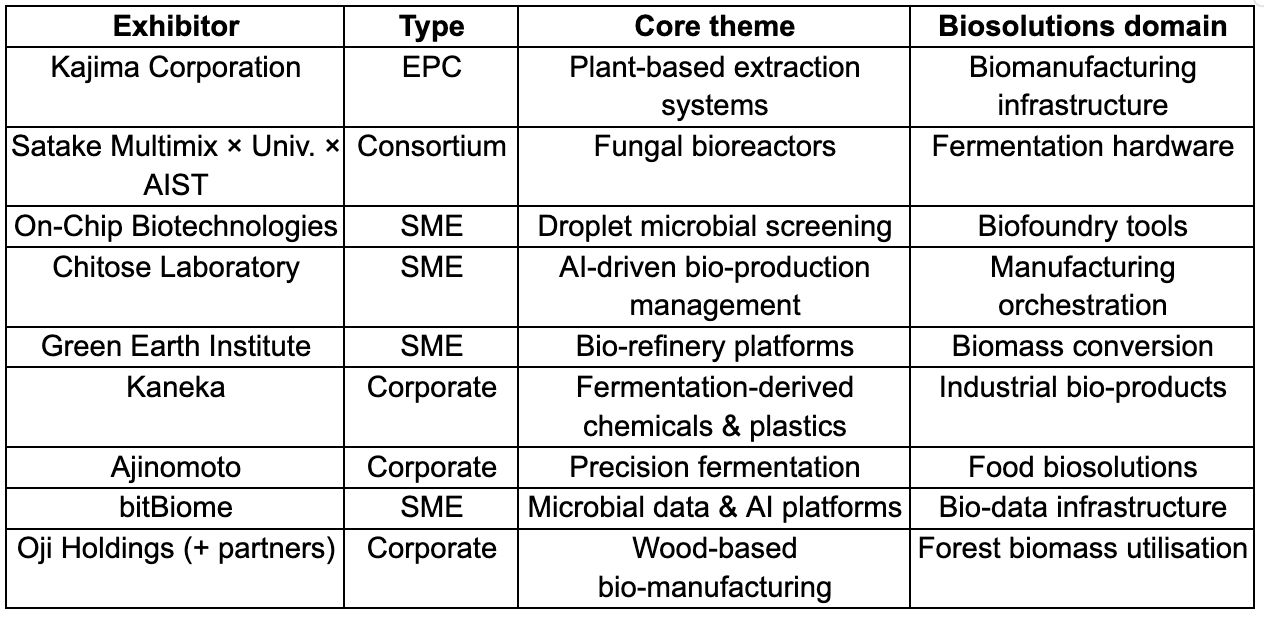

Public programmes coordinated through NEDO provide a window into how upstream innovation is supported beyond the laboratory.

Reviewing NEDO-supported exhibitors at BioJapan shows recurring characteristics across projects:

fermentation systems and bioreactors,

microbial and plant-based production platforms,

biomass, waste, and CO₂ utilisation,

bio-manufacturing infrastructure, analytics, and orchestration tools,

frequent use of multi-party consortia involving corporates, public institutes, and universities.

Examples of NEDO-supported biosolutions activities

NEDO-supported activity is largely oriented toward technical validation, platform development, and shared capability building, rather than company scaling or market expansion.

2.3 Early-stage capital and formation

Early-stage biosolutions activity in Japan is well supported, particularly at pre-seed and seed. Public agencies such as NEDO, AMED, and JST underwrite early technical risk through non-dilutive funding, complemented by in-kind university support and strategic corporate venture capital. A private VC layer exists but thins rapidly beyond the earliest stages.

Japan’s innovation base is therefore broad, applied, and validation-focused. The structural challenge lies not in invention, but in moving validated capability into coordinated industrial deployment and scale.

3. Corporate environment: appetite without a playbook

Japan’s corporates are genuinely engaged, not performatively. They show up early, they have industrial-scale assets, and they operate in exactly the markets where biosolutions is heading. And yet decisive scale-up leadership is rare. The interest is real; the playbook for acting on it isn’t.

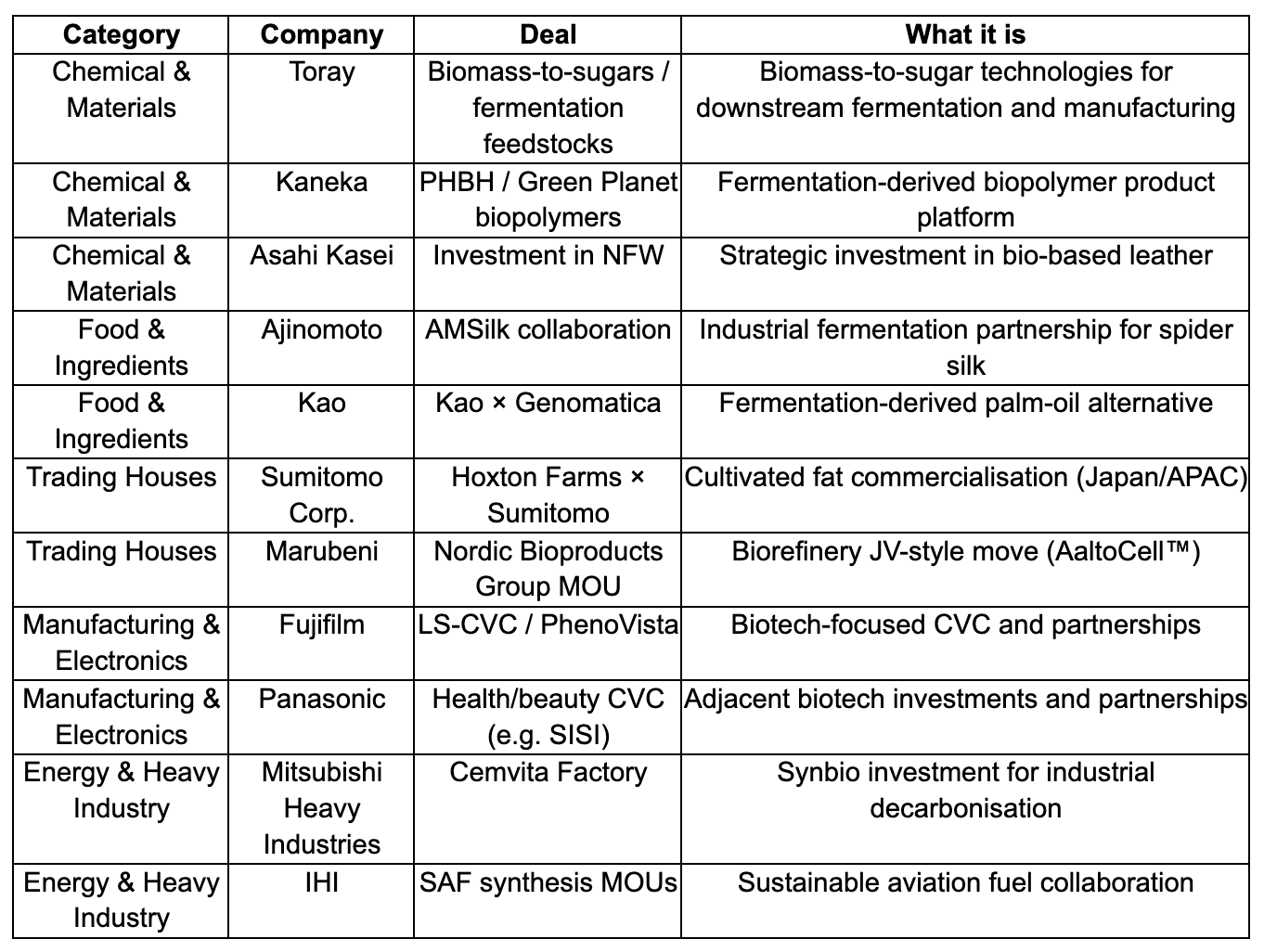

Across interviews and deal analysis, common patterns recur:

limited internal capability to integrate biosolutions across business units,

difficulty assigning ownership when technologies span divisions,

strong aversion to first-mover and reputational risk,

a default reliance on pilots, partnerships, or minority investments.

These behaviours are individually rational at the firm level, optimising for learning and downside protection, but collectively suboptimal at the system level when industrial adoption requires coordinated, multi-year commitment.

3.1 How corporates engage in practice

Corporate engagement is broad but appears to be typically framed around learning and risk management, rather than ownership of scale.

Even where CVC is involved, it functions primarily as a sensing mechanism to identify promising technologies, not a growth-stage anchor.

3.2 A structural advantage - and a gap

Japan holds a rare advantage: a deep late-stage applications environment in chemicals, materials, food, and manufacturing, aligned with the scales and timelines biosolutions require. Yet no mechanism reliably converts corporate interest into coordinated commitment.

Japanese corporates show strong appetite for biosolutions, but lack a shared playbook for integration and scale. The resulting gap between validated technology and industrial deployment persists, setting up the scale and coordination challenge addressed next.

Recent institutional moves reinforce this orientation toward collaboration, including a memorandum of understanding between UK Bioindustry Association and Japan Bioindustry Association, aimed at strengthening cooperation, information exchange, and industrial collaboration in bio-based industries.

4. Manufacturing capacity and regional leverage

From a manufacturing perspective, Japan retains significant manufacturing and process-engineering capability.

Domestically, there are multiple pilot-scale and demonstration facilities supporting fermentation, process optimisation, and early manufacturing. These are complemented by strong process engineering expertise embedded in both services firms and industrial incumbents. Examples include the Chiyoda Plant Biofoundry and Bacchus Bio Innovation.

Many Japanese corporates have deep ties to biomanufacturing sites in South East Asia and China. While cross-border scale-up introduces coordination, governance, and IP-control complexity, Japan’s regional industrial embeddedness provides credible pathways to reach scale.

In practice, Japan’s most distinctive advantage lies less in hosting all manufacturing domestically, and more in serving as an adoption, integration, and coordination node linking validated technologies to both domestic and regional scale pathways.

5. The Missing Middle: why validation doesn’t automatically become scale

The most consistent structural weakness identified across data and interviews is the growth-stage gap. However, this gap is not purely financial. It has three interlocking components:

Growth-stage capital and risk ownership

Industrialisation infrastructure and execution capability

Operator capability and experiential knowledge

5.1 Growth-stage capital and risk ownership

While early technical risk is well funded through NEDO, AMED, JST and early-stage VC/CVC, companies face significant difficulty once they must:

scale fermentation and downstream processing,

integrate with industrial customers,

expand internationally,

sustain multi-year burn during commercialisation.

Domestic Series B/C-scale venture capital remains limited. Corporate venture capital is typically structured for strategic learning and optionality rather than underwriting industrial scale. Public funding generally tapers once technical feasibility is demonstrated.

The resulting patterns are predictable:

early IPOs to access liquidity,

long-lived but sub-scale firms,

relocation to deeper capital markets,

gradual leakage of ownership and value creation offshore.

5.2 Industrialisation infrastructure and execution constraints

Feedback from ecosystem participants highlights a second layer of constraint: the practical realities of fermentation-based industrialisation in Japan.

Several structural challenges are present:

Limited access to low-cost fermentation feedstocks at global commodity scale has historically driven large amino-acid and fermentation plants to Southeast Asia and grain-producing regions rather than domestic sites.

Domestic fermentation expertise is concentrated within a small number of incumbents, while many new entrants lack large-scale operating experience, dedicated facilities, and sustained organisational commitment.

Industrialisation infrastructure remains incomplete, with few GMO-capable facilities, limited downstream processing (DSP) capacity, and public support still weighted toward upstream strain development rather than full-scale industrial readiness.

In practice, Japan supports invention and early technical validation effectively. It does not yet provide a fully integrated pathway covering strain → fermentation → downstream → qualification → industrial deployment.

5.3 Two manufacturing logics: local vs global

Fermentation production can broadly be divided into two categories:

Local production for local consumption

Mass production for global markets

From an economic security perspective, domestic manufacturing capacity remains strategically important for products consumed locally or embedded in critical supply chains.

However, for globally traded bio-based chemicals or intermediates, manufacturing economics often favour regions with abundant low-cost sugar, grain, or renewable energy inputs. Historically, Japanese fermentation leaders have located large-scale plants in Southeast Asia or North America for this reason.

This suggests that Japan’s long-term role in biosolutions manufacturing may not be binary (domestic vs offshore), but differentiated:

For strategic or domestically consumed products: strengthening local pilot, demo, and industrial infrastructure is critical.

For global commodity-scale products: Japan may function as an adoption, qualification, and integration node, while leveraging regional manufacturing capacity.

The structural opportunity therefore lies not only in expanding domestic fermentation capacity, but in coordinating technology development, corporate adoption, and regional manufacturing pathways.

5.4 Operator capability and experiential knowledge

Industrial fermentation and downstream processing are experiential as well as financial challenges. Large-scale deployment requires operators with practical scale-up expertise, which in Japan is concentrated within a small number of incumbents, often embedded in overseas plants. Many newer biosolutions firms lack this operating depth.

This concentration of expertise forms part of the “missing middle”: beyond capital and infrastructure, distributed operational capability is limited and must be deliberately mobilised for transition to scale.

5.5. What happens if nothing changes

This is worth dwelling on. If the structural gaps persist (and there’s no automatic reason they won’t) the trajectory is fairly clear: continued early liquidity events, high-potential firms relocating to deeper capital markets, and corporate adoption that stays permanently fragmented. Japan would remain a strong place to invent and validate. A disproportionate share of the value created from that invention would accrue elsewhere.

6. What could actually close the gap?

Taken together, the analysis suggests that Japan’s challenge is not invention. It is transition. Japan combines sustained applied innovation, strong public support for early translation, corporates with real downstream demand, and regional manufacturing embeddedness across Asia Pacific.

What is missing is an institution (or set of institutions) designed specifically to manage scale risk and industrial coordination.

Such an actor would not resemble traditional venture capital, nor a corporate incubator, nor a public R&D programme. Instead, it would operate at the interface of capital, infrastructure, and corporate integration.

Its functions could include:

Provide patient growth capital aligned with industrial timelines, supporting companies through scale-up to meaningful deployment.

Structure coordinated adoption frameworks with corporates, including offtake agreements, demand guarantees, and shared first-mover risk.

Integrate access to pilot and demonstration facilities, including GMO-capable infrastructure and downstream processing (DSP) capability, within commercialisation pathways.

Leverage regional manufacturing partners (e.g. Southeast Asia, Australia, North America) where economics favour external scale.

Crucially, this model would support horizontal division of labour and open innovation, rather than expecting each company or corporate to vertically integrate the full value chain internally.

6.1 Japan as an adoption and integration node

Under such a model, Japan need not compete directly with the United States in venture capital depth, nor replicate China’s state-directed scale-out model.

Instead, Japan could position itself as:

A site where biosolutions are validated in partnership with industrial incumbents.

A market where early corporate engagement reduces adoption risk.

A coordination hub linking platform technologies, downstream demand, and regional manufacturing networks.

A strategic manufacturing base for products where domestic production is economically and politically justified.

If coordination-first, growth-stage mechanisms were established (combining capital, industrialisation infrastructure, and corporate alignment) Japan could plausibly move from being primarily an execution layer to functioning as a centre of biosolutions adoption and scale within international value chains.

The primary opportunity now lies less in increasing invention and more in enabling this transition from validated capability to sustained industrial deployment.

6.2 Possible Institutional Forms

1. Public–private growth platform: A jointly capitalised vehicle combining government risk buffering with corporate and long-horizon private capital to support industrial scale-up.

2. Trading house–anchored consortium: Leveraging sōgō shōsha expertise in project finance, supply chains, and multi-party coordination to structure offtake, demand aggregation, and regional manufacturing partnerships.

3. Infrastructure-linked growth fund: A growth-stage investor directly coupled with pilot, demonstration, and downstream processing infrastructure to integrate capital with operational scale capability.

These models are not mutually exclusive, and the right answer likely depends on where appetite exists. The public-private platform requires government willingness to hold risk which is possible but slow. The trading house consortium is probably the fastest path to execution given sōgō shōsha already operate exactly this kind of multi-party coordination in other domains. The infrastructure-linked fund is the most capital-intensive but potentially the most durable. What all three share is the critical requirement: a coordinating actor willing to absorb first-mover risk rather than wait for someone else to go first.”

7. What this means for key stakeholders

Corporates: Participate in coordinated, risk-buffered adoption structures rather than attempting to lead scale-up independently.

Investors: Opportunity lies in growth-stage, coordination-first capital that underwrites industrial scale rather than rapid exits.

Policymakers: Early-stage support is effective; priority now is enabling scale through growth instruments, shared infrastructure, and policy backing for corporate participation.

Start-ups: Optimise for industrial fit and early corporate integration to de-risk deployment.

Cross-border partners: Engage Japan as an adoption and scale node within global biosolutions networks.

8. Conclusion

Japan’s biosolutions ecosystem has real structural strengths - and a specific, identifiable gap.

The innovation base is real. The corporate appetite is real. The downstream demand is real. That last point is worth pausing on: most biosolutions ecosystems are still trying to manufacture corporate interest. Japan already has it, embedded in industrial sectors with the scale and timelines that biosolutions actually require. That’s a harder thing to build than a funding programme or a pilot facility.

What remains to be built is the transition architecture that connects these pieces: patient capital, coordinated adoption, and the operational infrastructure to make scale-up something more than a theoretical possibility.

Whether that gets built (and by whom) is the open question. The pieces are there. The missing middle is a gap, not a ceiling.

Notes on Methodology

Company Data was provided in collaboration with One Nucleus

Patenting data provided by Potter Clarkson Law Firm and Ashley Evans, Inevus Advanced Analytics

BioSolution Deal History found through analysis of company press releases

Interviews were conducted as part of a broader campaign to understand the BioSolutions Ecosystem across APAC including policy makers, corporates, start-up operators and investors

Work supported by UK BioIndustry Association and Japan BioIndustry Association

Read More

Newletter & More

SynBioBeta

Join the innovators shaping the future with SynBio + AI. From health to ag, materials & more—be part of the revolution.